~ 2 min read

Using Excel to Calculate VaR for Your Portfolio

Using Excel to Calculate VaR for Your Portfolio

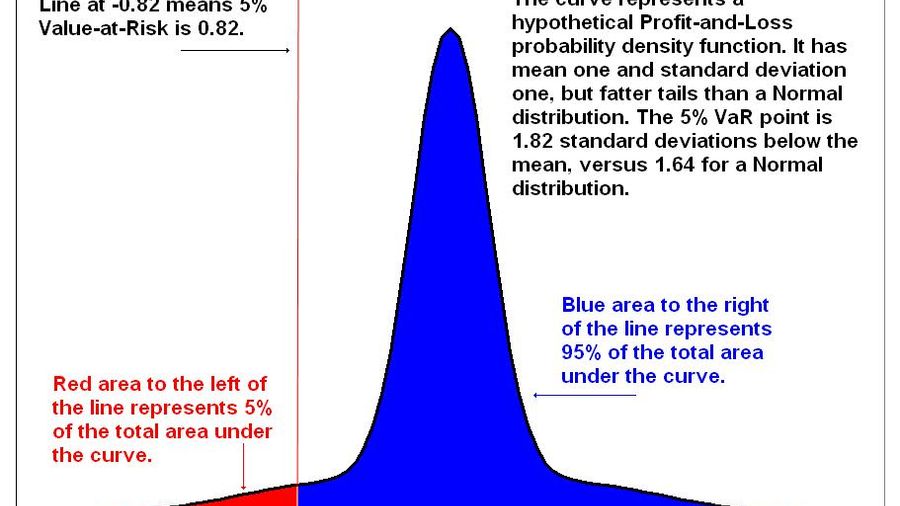

Value at Risk (VaR) is a measure of the risk of loss for a portfolio of investments. By using Excel's built-in NORM.INV function, investors can determine the maximum expected loss of their portfolio over a given time period, with a specified level of confidence. This information can be used to make informed decisions about portfolio management and risk management.

How to Calculate VaR in Excel

- Have your portfolio data in an Excel spreadsheet, including the names of each investment, the number of shares or units held, and the current market value of each investment.

- Decide on a time period and confidence level for your VaR calculation.

- Use the AVERAGE and STDEV functions in Excel to calculate the mean and standard deviation of your portfolio's returns.

- Determine the probability of a loss that corresponds to your chosen confidence level. For example, if you want to calculate a 95% confidence level VaR, the probability of a loss would be 1 - 0.95 = 0.05.

- Use the NORM.INV function to calculate the VaR value. The syntax for this function is:

=NORM.INV(probability, mean, standard deviation). Substituting the values you calculated for probability, mean, and standard deviation will give you the VaR value for your portfolio. - Use the VaR value to understand and manage the risk of your portfolio. For example, you can compare the VaR value to the expected returns of your portfolio to determine whether the potential loss is acceptable given the potential gain.

By following these steps, you can easily calculate VaR in Excel and use this information to make informed decisions about your investment portfolio. Additionally, you can use a tool like Gorilla Terminal to easily manage your portfolio and calculate VaR with just a few clicks, without the need for complex Excel formulas.