~ 2 min read

How to do Risk management with Value at risk(VaR) analysis

Risk management is the process of identifying, analyzing, and responding to potential risks in order to minimize their impact on an organization. One important tool used in risk management is the value at risk (VaR) calculation, which estimates the maximum loss that an investment portfolio is likely to incur over a given time horizon at a given confidence level.

The VaR calculation is based on the assumption that the returns of the portfolio are normally distributed, which means that they are symmetrical around the mean and follow a bell-shaped curve. This assumption allows for the calculation of the probability of a given loss, which is used to determine the VaR.

To calculate the VaR, we first need to determine the mean and standard deviation of the portfolio’s returns. The mean represents the expected return, while the standard deviation measures the amount of volatility or risk in the portfolio.

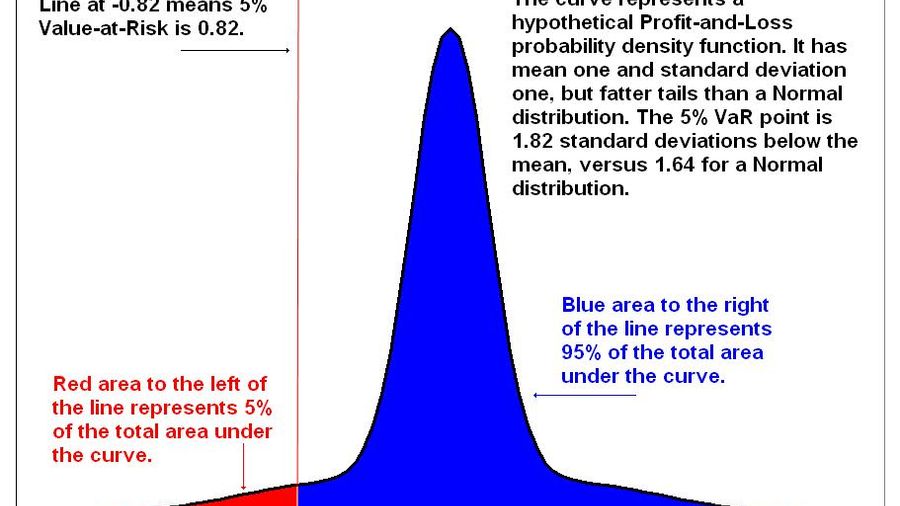

Once we have these values, we can use the normal distribution to determine the probability of a given loss. For example, if we have a confidence level of 95%, this means that we expect the portfolio to lose more than the calculated VaR only 5% of the time.

In addition to the normal distribution, the VaR calculation also takes into account the correlations between the different assets in the portfolio. A correlation matrix is used to measure the relationship between each pair of assets, with a value of 1 indicating a perfect positive correlation and a value of -1 indicating a perfect negative correlation.

The correlations are used to adjust the overall risk of the portfolio, as assets with a positive correlation will tend to move in the same direction, while assets with a negative correlation will tend to move in opposite directions. This means that a portfolio with a high degree of positive correlations will be more risky than a portfolio with a high degree of negative correlations.

Overall, the VaR calculation and correlation matrix are important tools for managing risk in an investment portfolio. By accurately estimating the potential losses and adjusting for the correlations between assets, organizations can make more informed decisions about their investments and minimize their exposure to risk.